What if you wake up one morning and receive mail that your service is no longer required at your office?

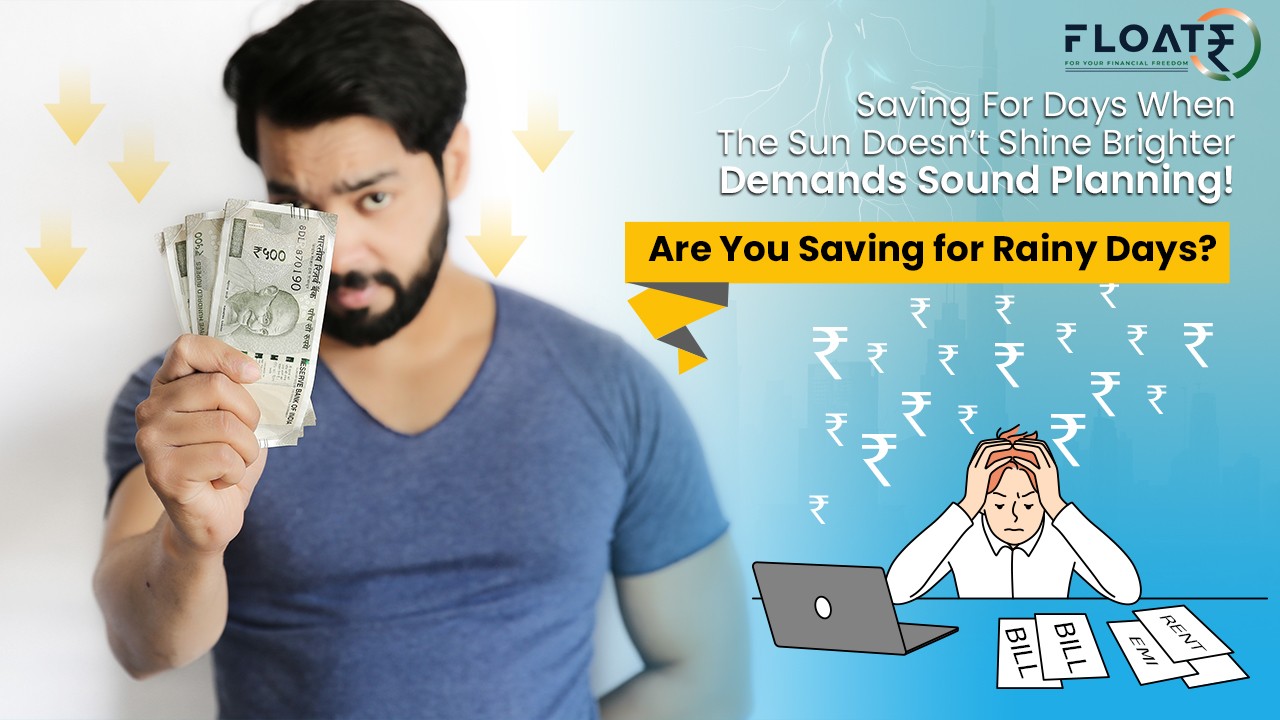

Are you ready to face the storm of rainy days with sound financial planning?

Life is unpredictable. Some days aren’t all sunshine, like when your car breaks down or your house needs a repair. Everyone encounters these situations at some point in their lives. That’s why it’s important to save while things are going well, so you’re protected when things go wrong. A rainy day fund can help you pay for unexpected bills beyond your normal living expenses.

Rainy day funds are set aside to take care of your monthly expenses + debts until you find another source of income. usually it should be somewhere 6 to 9 times of your monthly expenses including any loans.

What is the purpose of a rainy day fund? In the same way that you need to adjust your plans to accommodate unexpected weather, you should also have a financial backup in case of unexpected expenses. You might not anticipate a thunderstorm or a layoff, but either could happen at any time, so it’s best to prepare.

Looking at the current situation when even the giant companies are laying off, it’s a crucial step to save for rainy days. Not just in India, but globally IT layoffs have impacted more than 135,000 employees.

This recession is being followed by a pandemic, which has already caused immense stress on people globally and created almost a two-year-long period of increasing global uncertainty. And if the recession continues, there is going to be a definitive need for ensuring you take a relook at your finances.

Effective financial planning is extremely important, as managing finances and preparing for a rainy day can ensure you are secure no matter the situation. Be it an unforeseen expense, or a financial crisis – it is always important to make sustainable financial plans.

Once an individual gets a job, they should get insured with adequate insurance cover (life insurance and health insurance). This would help them to unburden themselves from expenses during a mishap. The second priority should be given to saving for rainy days for 6-9 months. After saving enough for those risky days, they can plan ahead for investing in mutual funds, pension schemes, equity, etc.

Let us look at some challenges in finance management

Monthly expenditure exceeding income: When your monthly needs and expenditure are more than the money you earn there is no scope for saving. Most people rely on EMI systems or Credit Cards but that is a hazard to effective financial management.

Living on borrowed expenses: One of the worst mistakes that people make is borrowing money from others. It is a vicious cycle and is never-ending where you borrow money, to pay others money. And should be avoided at all costs.

Not knowing how much you are saving: If you are unaware of the amount of money you save, you can never get hold of how much money you have or where your financial status stands. Financial status does not depend on how much you earn month on month but depends on how much savings you have.

Not knowing how to save: One of the biggest challenges is financial illiteracy. It is not only important to know how to earn money, but also know how to save. Understanding the different means and ways through which you can save money is extremely important and utilising them to work for you is essential.

Some people choose to save money rather than make investments. Savings, however, might not be sufficient to provide ongoing financial stability in a changing society. It might not be useful to keep idle money in bank accounts or lockers.

By increasing in value, investments may help reduce inflation. Compounding power aids in wealth building as well. Investing can also help you achieve long-term objectives like retirement planning, home ownership, and international travel.

Here are a few avenues for saving money:

- Fixed Deposits: One of the most popular investment options in India that offers a fixed rate of interest over a fixed period.

- Digital Gold: Gold has been amongst the most popular types of investment in India. As people are becoming more aware of the benefits of investing in digital gold, they are shifting to this option. One can invest in pure 24K digi gold without paying any making or wastage charges. On FLOATR, it starts with just Rs. 51!

- Mutual Funds: An excellent option for saving is mutual funds where there are options for lock-in periods or liquid funds that can be withdrawn anytime. One who is preparing to save for rainy days can start investing in mutual funds through SIP (Systematic Investment Plan) – investing a small amount of money periodically.

- Public Provident Fund and National Pension System: The PPF is a long-term savings plan supported by the Indian government with a 15-year lock-in period. PPF investments, however, are tax deductible and also rather secure. NPS (National Pension System) is a low-cost retirement option sponsored by the government. Any Indian citizen between the ages of 18 and 70 may choose to participate in the NPS program.

- Stocks: Stocks are risky but if well-planned can be effective in giving lifelong benefits to investors.

Here are some benefits of staying in control of your finances

- Staying in control helps you plan better for your future: By following correct financial management actions, defining a budget, and building a savings plan, you may forecast your income and saving capacities over time. This enables you to establish such plans and use them as inspiration to practise good budgeting and financial management.

- Reduce financial stress: Adults experience financial stress more frequently than any other type of stress. Money may not be able to make you happy, but it may help you sleep better at night and feel less stressed throughout the day.

- Being open to new opportunities: When your finances are in order, new opportunities may become available that were previously closed. Instead of focusing on the financial benefits, you may take advantage of the chance to examine new employment or career choices depending on what you’re most enthusiastic about.

- Being better prepared for uncertainties: When your finances are planned effectively, you can stay in control of your money and be better prepared for unforeseen situations.

How can you stay in control of your finances?

The world is going digital and having a digital partner to manage your finances is a good way to stay in control of your finances. FLOATR understands the challenges that a person faces while trying to stay in control. The biggest is trying to strike a balance between spending and saving.

FLOATR empowers individuals to achieve financial freedom by providing them with complete control of finance in an app-based system and also providing opportunities for financial management.

Here is what FLOATR offers:

Track Your Money!

FLOATR aids in preventing excessive spending and improper spending practices. You may record the areas where you spend the most money and compare your costs to your spending plan. By keeping track of your expenditures, you may reduce your expenses.

Achieve financial goals

With FLOATR, you may achieve financial freedom more quickly. You can also save for rainy days, develop a budget, set time-bound goals, allot money toward those goals, or invest in things like digital gold, equity baskets, mutual funds, fixed deposits, NPS, etc.

Insurance

What if a sudden mishap occurs? Would you break your savings or funds for that? A better option is to get insured or covered. FLOATR lets you save money and also choose the right insurance options for yourself. It also helps you plan and prepare for times of uncertainty. Begin your journey to financial freedom today.